Chargebacks are quite common, in the world of finance. They happen when customers raise concerns about a transaction on their credit card statement leading to the reversal of the payment. Chargebacks can be costly for merchants so it’s important for them to understand how they work and take steps to prevent them. In this article, we’ll provide a guide for merchants on dealing with chargebacks.

Important points: Chargeback Guide for Merchants

- A chargeback refers to a refund initiated by the bank in response to a disputed transaction by the cardholder.

- Chargebacks can result in losses. Harm a merchant’s reputation.

- Merchants can minimize chargebacks by implementing fraud prevention strategies and ensuring top-notch customer service.

Definition of Chargeback

A chargeback is essentially when a payment is reversed because a customer disputes a transaction mentioned on their credit card statement. There are reasons why chargebacks occur, such as fraud, unauthorized charges, merchandise or billing errors. When a chargeback is initiated, the payment gets reversed. The burden falls on the merchant to provide evidence countering that disputed claim.

The process of handling chargebacks involves parties that include the cardholder, the merchant, the bank (that processes payments, for merchants), and the issuing bank (that issued the credit card). The cardholder initiates the chargeback with their issuing bank who then communicates with the acquiring bank before reaching out to notify the merchant involved.

Merchants have to present evidence to challenge a disputed charge. If the evidence is insufficient the chargeback remains valid. The payment is reversed.

Reasons for Chargebacks

There are common reasons why customers may initiate chargebacks. These include instances of fraud, unauthorized charges, defective products, and billing mistakes. For instance, a customer might dispute a charge if they didn’t receive the ordered merchandise or if it was faulty. Similarly, a customer could contest a charge if they didn’t authorize the transaction or believe they were overcharged.

Chargebacks can be expensive for merchants. Can harm their reputation. To prevent them merchants should ensure that their products and services meet customer expectations provide customer service and implement fraud prevention measures.

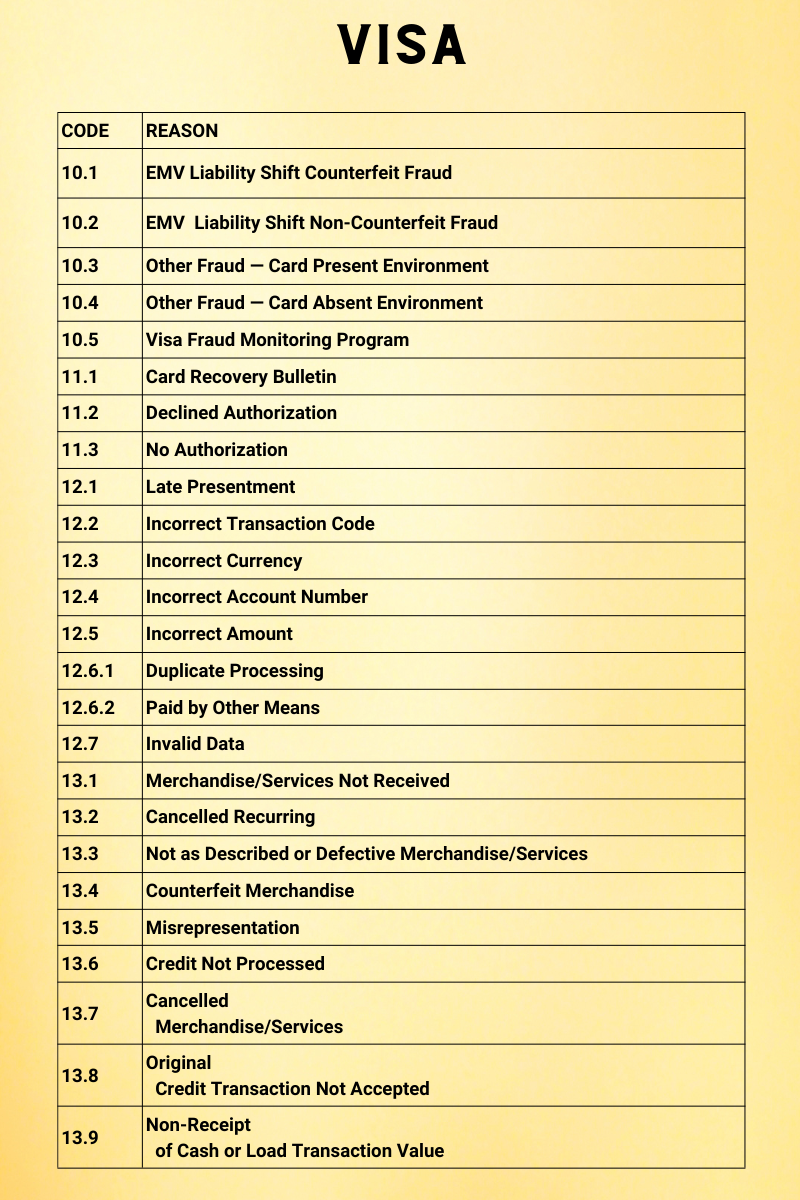

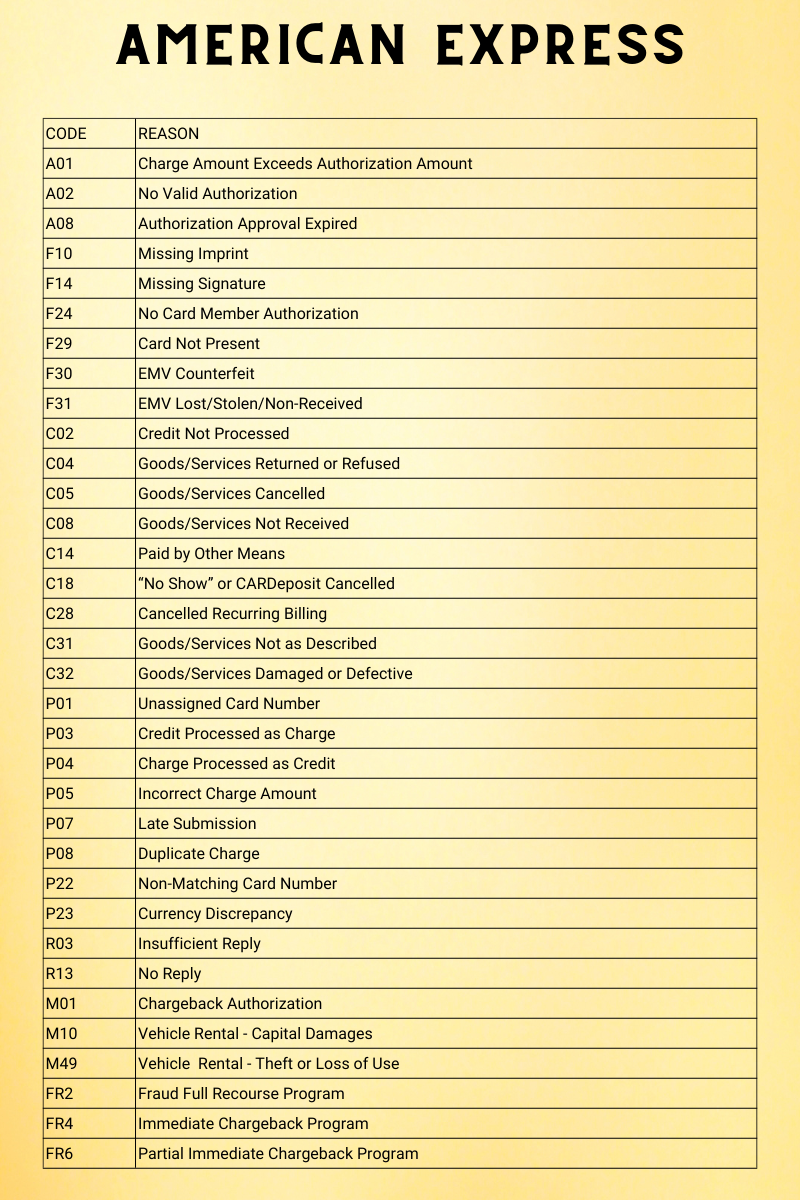

Here is a list of all chargeback codes used by different credit card networks.

Differentiating Between Chargebacks and Refunds

A refund is when a merchant voluntarily returns funds to a customer. In contrast, a chargeback is initiated by the customer requiring the merchant to dispute the charge. While refunds are typically initiated by merchants themselves chargebacks are initiated by customers who must provide evidence, for their dispute.

Refunds are usually issued in cases where customers express dissatisfaction, with a product or service or if the product or service turns out to be defective. On the other hand, chargebacks are typically initiated when customers suspect they have fallen victim to fraud or when they did not authorize a transaction.

Credit Card Chargebacks Vs. Debit Card Chargebacks

When it comes to debit card and credit card chargebacks the process is quite similar. However, there are some differences one should know. For instance, debit card chargebacks may take longer to process due to the withdrawal of funds from the customer’s account. In contrast, credit card chargebacks might be processed swiftly as funds are not immediately withdrawn from the customer’s account.

Another significant distinction lies in the regulations governing debit card and credit card chargebacks. Debit card chargebacks may be subject to regulations that differ from those of credit cards. For example, under the Electronic Fund Transfer Act (EFTA) consumers using debit cards enjoy more protections such as their right to dispute unauthorized charges.

History Of Chargebacks

The concept of chargebacks has been in existence, for decades. It was initially introduced as a means of safeguarding consumers against fraudulent charges. The first set of regulations about chargebacks was implemented during the 1970s with an aim to protect individuals who fell prey to credit card fraud.

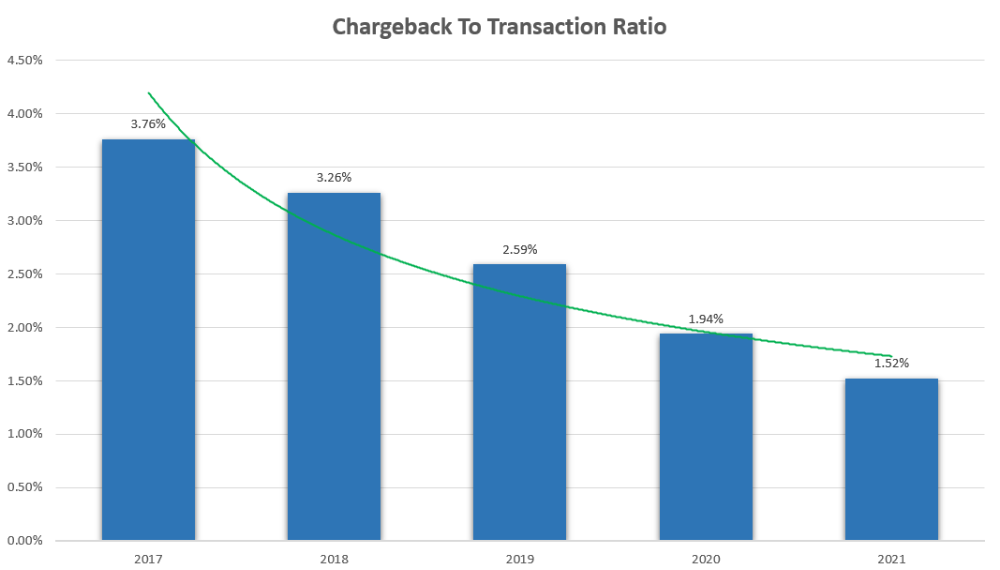

Over time the process of chargebacks has evolved to include a range of disputes, including issues related to the quality of merchandise, shipping problems, and billing errors. Nowadays chargebacks have become quite common in the e-commerce industry. Recurrent chargebacks can harm the reputation of any merchant.

Understanding the Process of Chargebacks

The chargeback process involves certain different steps a merchant should understand. It begins when a customer raises a dispute regarding a transaction with their bank. The customer’s bank then contacts the acquiring bank, which subsequently reaches out to the merchant involved. In order to challenge the disputed charge, the merchant must provide supporting evidence. If this evidence is deemed insufficient the chargeback is. Payment is reversed.

Completing the chargeback process can take weeks. Prove expensive for merchants. To prevent occurrences merchants should implement measures aimed at fraud prevention while also delivering customer service and ensuring that their products and services meet customer expectations.

When Can Consumers Utilize Chargebacks?

Consumers have situations where they may choose to utilize chargebacks. Some instances may be

- If they fail to receive the ordered merchandise.

- If there are defects in the product.

- If consumers did not authorize a transaction.

- If the consumer finds the charges fraudulent.

Are there any situations where consumers are not eligible, for chargebacks?

Yes, there are various scenarios where the consumer is not eligible. But, there are two important situations as mentioned below

- If the customer receives the merchandise as described and it is not defective, they may not be eligible for a chargeback.

- If the customer has authorized the transaction themselves, they may not qualify for a chargeback.

What about cases of chargeback fraud?

Deliberate chargeback fraud occurs when customers intentionally initiate a chargeback in order to deceive the merchant. This could happen when customers receive the merchandise and then dispute the charges or falsely claim that they never received the merchandise that was actually delivered to them.

Merchants can prevent chargeback fraud by implementing fraud measures such as requiring delivery signatures, tracking shipments and verifying billing addresses.

Impact of Chargebacks on The Merchant

Merchants should be aware that chargebacks can result in both losses and damage to their reputations. They might incur fees associated with chargebacks. Will need to provide evidence to contest them. If their evidence is deemed insufficient the charge will be paid back to the customer.

Apart from losses, chargebacks can also have an impact on a merchant’s reputation. Customers may be hesitant to continue doing business with a merchant who frequently experiences chargebacks. In a few cases, merchants might find themselves added to chargeback monitoring programs.

Impact of Chargebacks on The Consumer

Chargebacks are not without consequences for consumers either. Initiating a chargeback can have effects on an individual’s credit score. Even lead to the cancellation of their credit card in some rare cases. Therefore, it is advisable for consumers to only resort to chargebacks when they have reasons and should attempt to resolve any issues with the merchant before initiating the chargeback process.

So, Who Is Mainly Responsible for Chargebacks?

Determining responsibility for chargebacks can vary depending on the circumstances of each transaction. Generally speaking, if a merchant fails to provide evidence against a disputed charge, they will be held accountable for the chargeback. However, in cases where fraud is involved the issuing bank may assume responsibility for the chargeback.

Merchants have ways in which they can proactively prevent chargebacks. This includes implementing fraud prevention measures and offering the best customer services. Additionally ensuring that products and services consistently meet customer expectations is crucial.

It is important for the merchant to have clear and transparent policies for returns and refunds. They should take every step to ensure that the customer is aware about these policies. This will help to resolve the chargeback issues with the customer easily.

Understanding Chargebacks with A Real-Life Case Study

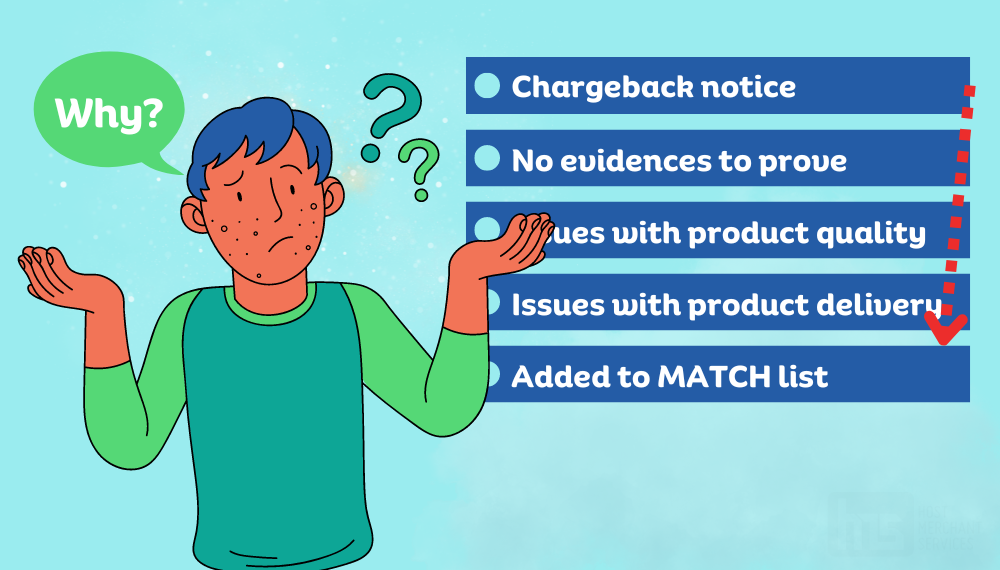

To illustrate how bad the impact of chargebacks can prove to the merchant let us consider John’s case. John is a business owner who had been operating his store successfully for two years.

One day he received a notification regarding a customer who had requested a refund due, to a discrepancy in the product they received. The customer claimed that the item did not match the description provided.

John was confident that he had shipped the product. Unfortunately, he lacked concrete evidence to support his claim. Moreover, he was unsure about the steps to dispute chargebacks. Consequently, he initially chose to overlook it assuming it was a one-time incident.

However, this turned out to be the start of his troubles. In the coming months, John encountered additional chargebacks specifically related to issues with product quality and delivery. The impact on his business became significant as he not only faced losses for “faulty” goods but also incurred fees associated with each chargeback.

Eventually, Johns’s payment processor took notice of the number of chargebacks. Imposed fines and penalties on his account. Additionally, they added him to their MATCH list – a database that compiles information about merchants, with chargeback rates – which made finding another payment processor quite challenging.

John came to realize that disregarding these chargebacks had been a huge mistake.

He started to take proactive measures to prevent chargebacks, such as improving product descriptions, providing better customer service, and using a fraud prevention service. He also learned how to dispute chargebacks and respond promptly to any notifications.

Ultimately John managed to decrease his chargeback rate and safeguard his business from further losses. He learned the hard way that merchants cannot afford to neglect chargebacks.

If you are a merchant then John’s case will give you an insight of the losses and reputation you might face if you ignored chargebacks.

Regulations Regarding Chargebacks

There are regulations and guidelines, in place governing chargebacks, which include thresholds for chargebacks and time limits for disputing them. Merchants should familiarize themselves with these regulations. As a merchant, you should take all the measures to ensure compliance.

Chargeback Services

Merchants can avail of chargeback services, such as third-party providers specializing in dispute resolution and fraud prevention. It is crucial for merchants to conduct research on these services and select a provider that can easily handle their requirements.

Conclusion

Chargebacks can prove costly for merchants. It can harm the reputation too. Having an understanding of how chargebacks function can help in preventing loss of money and reputation.

Merchants should implement fraud prevention measures, deliver high-quality customer service, and ensure that their products or services meet customer expectations in order to minimize chargebacks. By following these any merchant can prevent undue losses by chargebacks.

Frequently Asked Questions (FAQs)

1. What is a chargeback? Why is it significant?

A chargeback refers to the reversal of a credit card transaction. It holds significance as it has the potential to impact your business and financial stability.

2. Who has the authority to initiate a chargeback and under what circumstances?

Customers have the option to initiate a chargeback, in cases where they suspect fraudulent activity or if they haven’t received the promised goods or services.

3. How can I avoid chargebacks?

To avoid chargebacks, it is important to ensure that your product descriptions are clear and accurate. You should respond promptly to customer inquiries and swiftly resolve any issues.

4. What happens if I receive a chargeback?

When you encounter a chargeback the funds from the sale will be temporarily withheld until the dispute is resolved. Additionally, there might be a fee associated with it.

5. How much time does it take to resolve a chargeback?

The time required to resolve a chargeback can vary depending on the complexity of the case. If a merchant or the customer can produce strong evidence the issue is resolved quickly. Anyhow, it could take anywhere from a few weeks to a few months.

6. My customer made a false chargeback claim. What should I do?

In situations where you believe that a customer’s claim is false, you have the option to challenge the chargeback. However, before you challenge you should ensure that you have all the evidence to prove the claim as false or fraudulent.